The Transaction Blind Spot

Why PSPs and Gambling Operators Are Missing Fraud at the Moment That Matters Most.

Fraud prevention has a timing problem. Not a data problem. Not necessarily a tooling problem. A timing problem.

Across the payments ecosystem, PSPs and gambling operators are generating more risk intelligence than ever before. Every login, deposit, device change, IP shift, velocity spike, withdrawal request, wallet interaction, and gameplay action creates another layer of customer insight.

Yet despite all this visibility, fraud still succeeds at the exact moment it matters most: when the transaction occurs.

This is the operational blind spot quietly reshaping financial risk across digital payments.

The industry spent years investing heavily in onboarding controls. Identity verification became stronger. KYC orchestration matured. Document verification, biometric liveness, sanctions screening, and AML monitoring all evolved rapidly.

But fraud operations evolved with it.

Fraudsters Are Exploiting Trust, Not Just Identity

Sophisticated fraud rings no longer rely solely on fake identities or instant account abuse. They now focus on lifecycle manipulation, behaving normally long enough to avoid friction, then exploiting the transaction layer when exposure is highest. Some even temporarily absorb small losses to strengthen account credibility before later initiating larger transaction abuse.

A customer may appear completely legitimate for weeks before exhibiting risk behavior. Then suddenly:

- Withdrawal velocity spikes

- Linked accounts begin behaving similarly

- Payment methods rotate rapidly

- Wallet movement accelerates

- Transaction patterns shift dramatically

- Coordinated payout activity appears across multiple accounts

“The modern fraudster understands transaction timing better than many fraud systems do. By the time disconnected systems correlate suspicious activity across deposits, devices, wallets, and withdrawals, the funds are often already gone. The fraud was technically detected. It was just not stopped,” states Alfredo Solis, Managing Director, AcuityTec.

The Operational Blind Spot Inside PSP and Operator Environments

The speed of modern payments has fundamentally changed the economics of fraud response.

Instant payment rails, real-time wallet activity, and faster payout expectations have dramatically compressed the time available to identify and interrupt suspicious behavior. The faster the payment ecosystem becomes, the smaller the fraud response window becomes. This results in a fraud ecosystem that is increasingly fragmented. According to the Merchant Risk Council’s 2025 Global eCommerce Payments & Fraud Report, organizations now rely on an average of five fraud prevention tools simultaneously to manage the operational complexity of modern-day transactional fraud.

Solis comments, “No longer can organizations manage fraud effectively through disconnected operational systems where KYC operates in one environment while transaction monitoring, device intelligence, payment fraud monitoring, and chargeback management exist across separate operational layers.

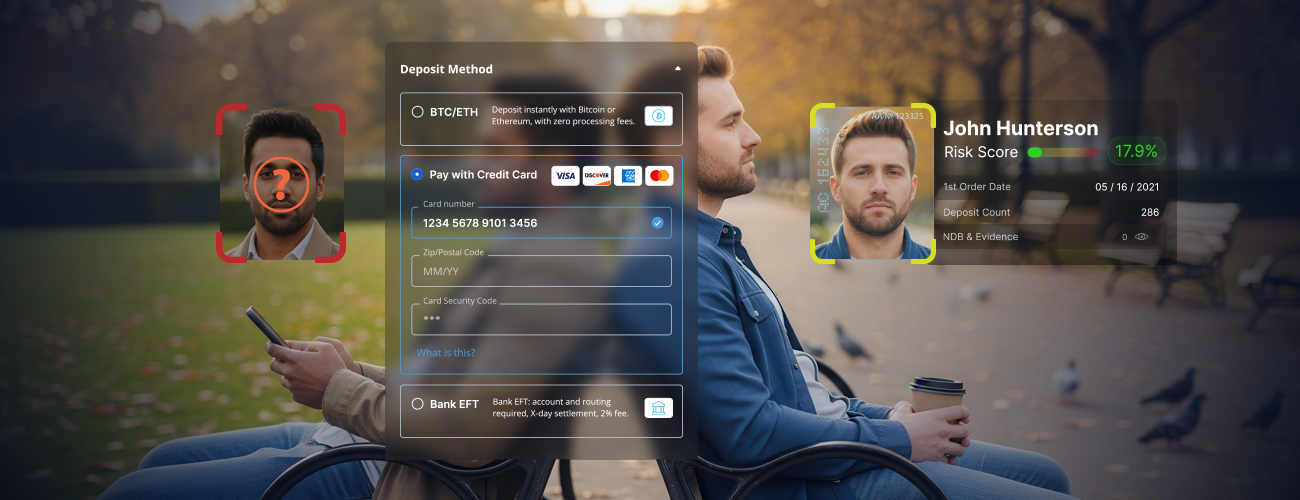

“Individually, each system may perform well. The problem is that fraud does not occur in isolation. Deposits, wallet activity, payment methods, linked accounts, and withdrawals are interconnected risk events that unfold simultaneously across the customer lifecycle. These signals cannot be evaluated independently. They need to be unified as part of a connected transaction intelligence like AcuityTec, capable of identifying and interrupting suspicious behavior in real time.”

The Future of Fraud Prevention Is Transaction Timing

According to the 2026 AFP Payments Fraud and Control Survey, 76% of organizations reported attempted or actual payments fraud in 2025. Additionally, Reuters reports that U.S. online gambling operators are facing increasing scrutiny over their ability to identify suspicious transactional behavior after account onboarding. Highlighting the market's need to rapidly shift towards embedded holistic transaction intelligence rather than isolated fraud tooling.

"The reality is that most fraud losses don't occur because operators missed a risk signal. They occur because the signal wasn't connected to the transaction quickly enough," states Alfredo.

“At AcuityTec, our focus is on helping PSPs and gambling operators close the transaction timing gap by embedding real-time risk intelligence directly into payment and withdrawal decisioning workflows, rather than relying solely on trust established during onboarding. Dynamic pKYC can be triggered automatically during high-value transactions, withdrawals, or other suspicious events, ensuring customer trust is continuously reassessed as risk evolves.

“Our real-time risk intelligence continuously evaluates account behavior across device intelligence, transaction velocity, payment methods, deposit-to-withdrawal patterns, linked account activity, behavioral anomalies, and pKYC events to generate a unified, continuously evolving risk score. When suspicious activity or coordinated account behavior is identified, alerts, step-up verification, or automated risk actions can be triggered immediately, enabling operators to intervene before fraudulent transactions are completed and funds leave the ecosystem.”

As fraud continues to evolve beyond onboarding and deeper into the transaction lifecycle, the future of fraud prevention belongs to organizations that can turn intelligence into action before a transaction becomes a loss.

To learn more or discuss your transaction risk challenges, book an intro call with the AcuityTec team.